This post may include affiliate links. Please read the disclosure at the bottom of our “About” page to learn more about our affiliate program.

If you’re a college student, you’ve obviously got a lot on your plate. You’re trying to pass all your classes. You’re figuring out your schedule for the next semester. You’re dealing with your annoying roommate. And, if you’re anything at all like I was when I was in school, every so often you freak out a little bit about your money situation. But with more pressing matters at hand, it’s easier to just push the money stuff off for now—there’s plenty of time for that later, right?

While it’s true that life is a long journey, this thinking can actually set you up for a lifetime of financial hurt. The earlier you can start investing, paying off your student loans, and building up your savings, the more time you have to allow your money to work in your favor. Waiting until after graduation to get your finances under control, while easy in the moment, certainly isn’t what you should do.

So what should you do? It really only takes a few hours to get your finances in order, and once the groundwork is done, it takes just a few minutes each month to make sure you’re staying on track. The simple money steps that all college students should take are things like:

- Organizing and keeping track of your student loans in a spreadsheet like this one

- Figuring out a simple weekly and monthly budget so that you know how much money you have coming in and what you are spending it on

- Once you know where your money is going, figure out ways to trim your expenses so you can free up some extra cash

- Use that extra money to start saving and investing for your goals, and to pay down your student loans (or other debt) faster

In the past, going through this whole process from start to finish could easily have taken an entire day to go through and get started. But with all of the technology and tools available to college students and graduates today, this really is something you can do on a Saturday afternoon after you’ve finished your weekend reading and before you head out to the bars.

To make the process of getting started a little easier, I thought that it would be a good idea to pull together a list of the most helpful money tools for college students. Below, you’ll find apps that can help you figure out your budget, apps that can help you start investing, apps that can help you bolster your savings, and apps that can help you make some extra cash.

Best Apps for Investing

Investing, at its heart, means taking money you have now and putting it to work to make more money that you can use in the future. Though retirement is probably “The Goal” that people think of when they think of investing, the truth is, you can invest for short-, mid-, and long-term goals—everything from saving up for a car, stockpiling a down payment for a house, or sending your future children to college debt-free. Below are some apps that you can use to learn the basics of investing and get off on the right foot.

Acorns

The Acorns investment app is an amazing way for newbie investors to get started investing, and offers a number of ways for users to start building an investment portfolio. I personally use Acorns and love it, so I’ve written about it a whole bunch in the past.

Long story short, when you sign up for the app you choose a portfolio from conservative to moderate to aggressive, and then can begin investing with as little as $5. All of the portfolios are completely diversified to offer you exposure to the market through a number of ETFs. You can contribute money directly, through the app’s “round ups” feature, through their Found Money program, or by referring friends. And though it’s not yet active, you will soon even be able to open an IRA through Acorns to fund your retirement.

The best part? You’ll pay a low fee of $1 each month for accounts up to $1,000,000. Oh, and college students can use the app for free for four years. Give it a try by clicking here.

Stash

Stash in an app much like Acorns in that it takes just $5 to begin investing. But whereas Acorns comes with limits in terms of portfolio options (you currently have just 5 portfolios to choose from if you’re an Acorns customer), Stash offers more than 40 portfolio options to choose from, giving you a bit more control of where your money is going. All of the portfolios offered through Stash are built from ETFs, meaning they come with built-in diversification, and are arranged by “themes” like:

- Standard “Mixes” that are broad groupings of Conservative, Moderate, and Aggressive diversification, much like Acorns

- Delicious Dividends, which invests heavily in dividend stocks

- Internet Titans, which invests heavily in technology stocks

- Up-and-Coming, which invests in emerging markets

- Clean & Green, which invests in clean energy companies

- And a whole lot more

You can make one-time lump-sum investments or use the app to build an automatic investment schedule (what they call “Auto-Stash”) on a weekly basis.

Want to take your investment portfolio into your own hands instead of selecting a pre-made portfolio? With Stash, you have that option, too. Stash now allows investors to choose from more than 95 individual company stocks (as of September 2018), including favorites such as Walmart, Visa, Disney, Coca-Cola, Tesla, Starbucks, and more.

The price to use Stash is identical to the pricing that Acorns uses: $1/month for accounts under $5,000 ($2/month for retirement accounts under $5,000) and 0.25% for accounts over $5,000. You can try Stash out by clicking here, or read my full review of Stash here.

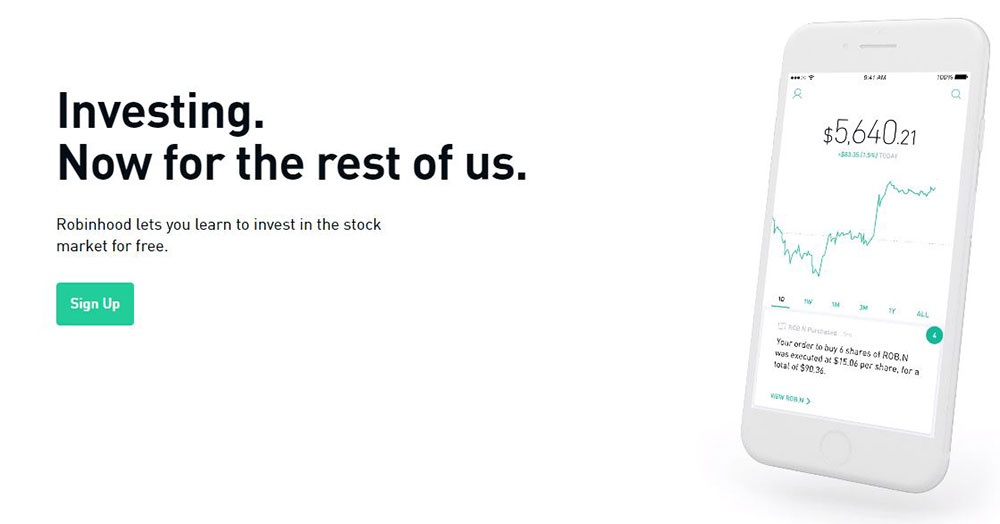

Robinhood

Robinhood is an investment app that lets you buy and sell stocks free of charge. Where it differs from Acorns and Stash is that, instead of buying into pre-made portfolios, Robinhood customers purchase only the stocks and bonds that they want and believe in. You can do this by choosing individual companies, or you can purchase from “Collections,” which are sort of similar to Stash’s “Themes.” Collections include things like Gas and Oil, Entertainment, and Social Networks, as well as categories curated by Robinhood staff like 2017 IPOs and Female CEOs. In addition to investing in stocks and bonds, you can also invest in Cryptocurrencies like Bitcoin, Ether, and more now that Robinhood has launched Robinhood Crypto.

So you’re probably wondering: How does Robinhood make money? It does in two ways. The first is that it collects interest on money that is left in your brokerage account but not invested (much like how a bank operates). It also makes money through Robinhood Gold, its premium version designed more for professional traders than for newbies.

Best Apps for Saving Money

A lot of people fall into the trap of only saving whatever they have leftover at the end of each week or month. Unfortunately, for a lot of us, when we go this route the amount saved ends up being zero. That’s why it’s important for you to pay yourself first: That way, you’ll know that you’re working towards your financial goals, even when your budget is tight. These apps will help make it easier to start saving, even if you don’t think you have the room in your budget.

Stash

Like we mentioned above, Stash offers both investment and savings options. See the description above for more details!

Digit

Digit is an app that aims to use machine learning to automatically analyze your spending habits and transfer money from your checking account to your savings account—every day! It works by analyzing your income and spending and finding times where it can transfer funds that you don’t need and won’t miss. Because most of us only save what we have left at the end of the month, we often end up saving nothing; Digit’s mission is to fix that problem.

Because Digit isn’t a bank, it can’t pay you interest. Instead, every three months you save with Digit, you’ll receive a 1% “Saving Bonus,” which is, in essence, interest on the funds that you’ve transferred and held in your Digit account. Same thing, different name.

You can try Digit for free for 100 days. After that, you’ll have to pay $2.99/month. Click here to try Digit.

ChangEd

If you’re familiar with Acorns, then you know how spare change “round ups” work: You make a purchase, and the app rounds up to the nearest dollar, and sets that extra cash aside. (For example, if you buy a $0.75 pack of gum, the app withdraws an extra $0.25 from your checking account, bringing your total spend to $1.)

But whereas Acorns uses the extra spare change to help you start investing, ChangEd uses the money to help you pay down your student loans more quickly. Once the app has helped you set aside $100, the money is instantly applied to your student loan principal as an extra payment, helping you save money and get debt free faster.

And it costs just $1 a month to sign up. Not too bad for giving you an extra weapon to wield in your battle against student loans.

Simple

Simple is a relative newcomer to the world of online banking. In the simplest terms, Simple is an app-based checking account that allows you to track your spending and budget for regular expenses and savings goals automatically, making it easier than ever for you to stay on track financially.

In addition to all of those awesome features, Simple is completely fee-free, allowing college students (and everyone else) to save a lot of money compared to most big banks. With Simple, you’ll never pay monthly maintenance fees, overdraft fees, transfer fees, card replacement fees, or fees for your account dropping too low. The app even comes with a built-in ATM finder to help you find more than 40,000 ATMs that are a part of Simple’s fee-free network.

I personally love Simple, and I think you will too. If you’re interested in learning more, I wrote this review of the Simple banking app that looks at the company in closer detail.

Pluto Money App

Pluto is a money management app that was created specifically to appeal to Generation Z (though it is also used by others) and to help members of that generation identify and reach their money goals.

Using behavioral science and data analysis, the app was built to guide users towards their financial goals—first by helping them identify these goals, and then by suggesting spending challenges to help the user reach those goals. Challenges are tailored by the users’ unique spending habits to ensure that they are relevant and actionable, and are typically designed to either help a user cut their spending or actively save more money.

Though still relatively new, Pluto has potential to be a real game changer for college students and others just starting to dip their toes into the world of personal finance. Read our full review of Pluto here.

Ally Mobile

Ally is a real standout in the world of banking, for one simple reason: They pay some of the best interest rates around. Currently, if you’ve got an Ally savings account, you’ll receive an impressive 1.85% APY on your money. Ally can afford to pay such high rates because it is a predominantly online company, allowing it to slash many of the expenses that traditional brick-and-mortar banks have to pay. That means fewer fees for you, and a greater piece of the interest pie.

One of my favorite features of banking with Ally is the fact that it’s extremely easy to open multiple accounts, which you can name and use to save for different goals. Whether you need to set aside funds for taxes, build an emergency fund, save for a large purchase, or maybe even save for a vacation, Ally will help you set aside and grow your money much more easily than other banks.

In addition to savings accounts, you can use the Ally Mobile app for checking and for investing in certificates of deposit (CDs). Just like their savings rates, Ally’s checking accounts and CDs offer above-average return for users.

Best Apps for Budgeting

If you don’t know how much money you have coming in and where you’re spending it, then there’s no way you’ll be able to work towards other financial goals like investing and saving. That’s why budgeting is so important—for college students, and everyone else!

Here are some apps that can help you set up a budget that you can stick to.

Mint and Personal Capital

When you’ve got multiple student loans, a checking account, a savings account, and a credit card, finances can get pretty complicated. Add in things like investment accounts, car loans, and other debts, and it can be downright impossible to manage. How do you keep track of so many different accounts? How will you ever truly know how much money you have, how much money you owe (and to who), and how your investments are doing?

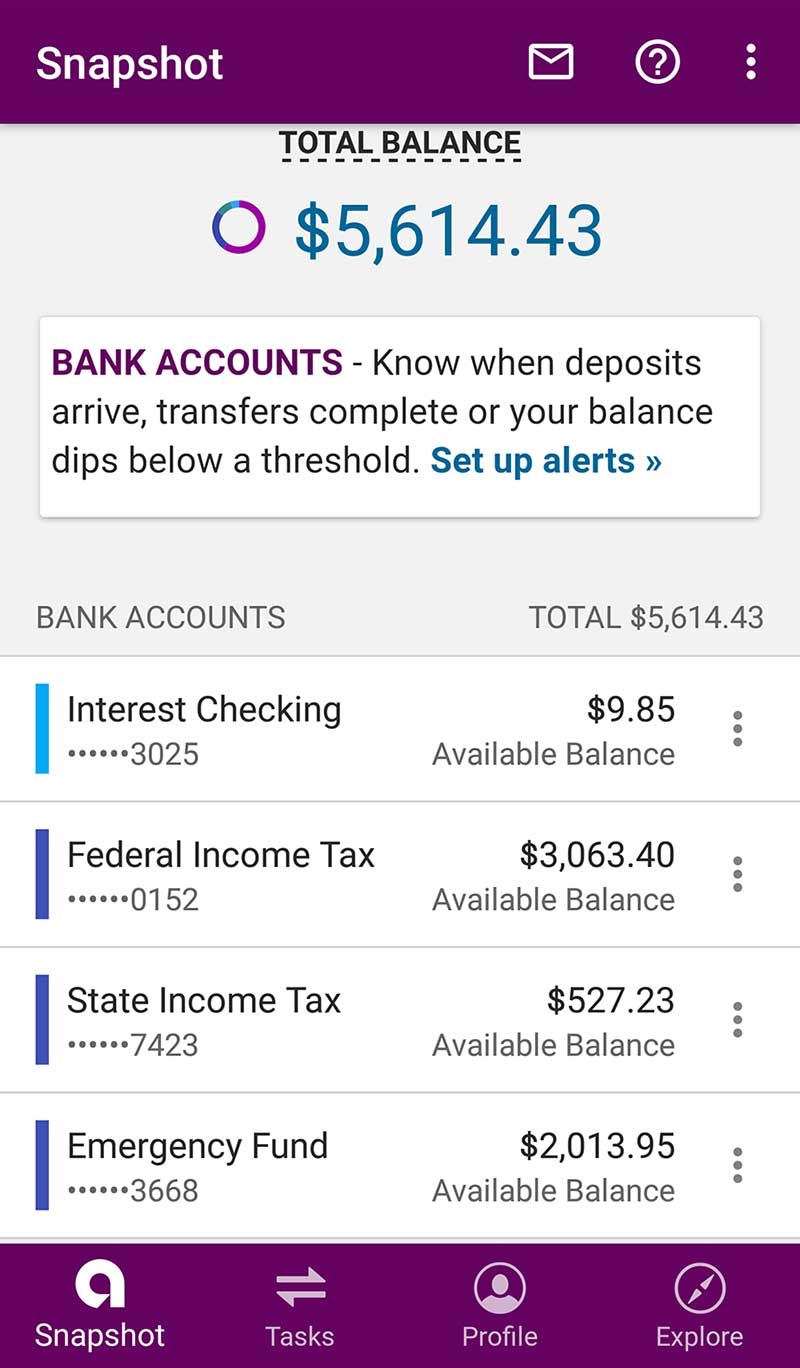

Mint and Personal Capital are two apps that aim to solve this problem by making it easier for you to get a clear snapshot of your complete financial situation. I’m calling them “budgeting apps” here, but in reality, they are “financial health apps.” And that makes them really powerful.

Both of these apps work in pretty much the same way: You link all of your financial accounts through their secured systems. The app then pulls your financial data when you log in, ensuring that you always have the most up-to-date data available. You can then use this information to analyze and plan your spending so that you are putting your money to better use.

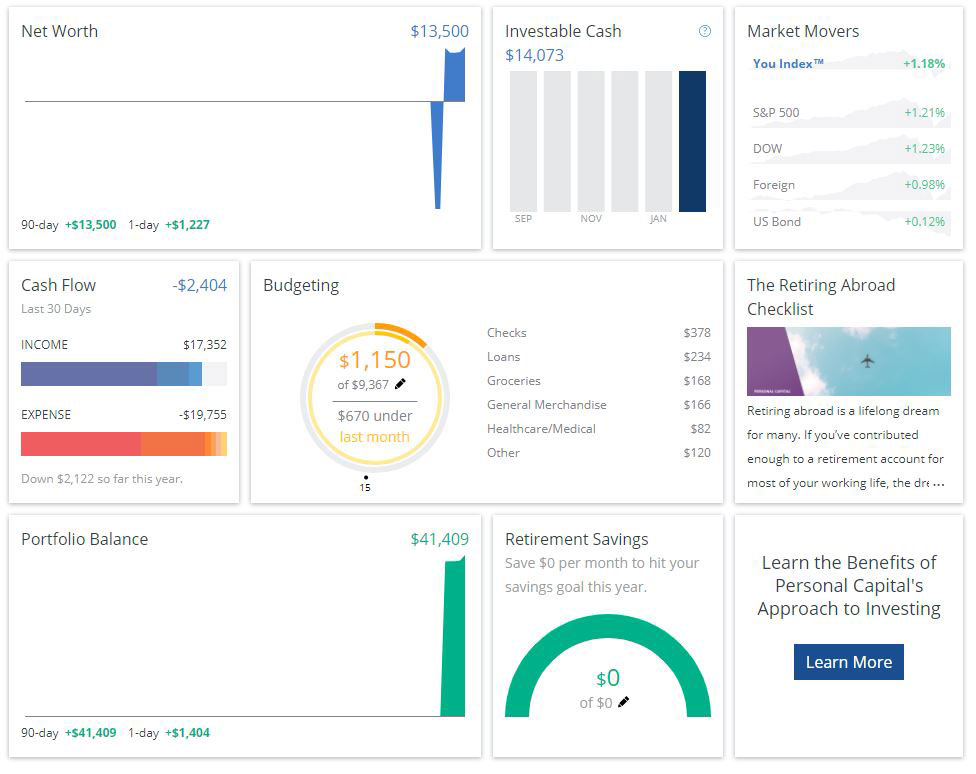

Personal Capital‘s real strength is in its all-in-one dashboard (below) that shows you all of your financial data in one place, letting you quickly and easily know what your money is doing. It’s the primary reason that I use the app personally. The app will also notify you if it notices changes to your income flow or spending habits, guiding you along to financial independence. (For example, when I logged in the other day the app notified me that I was running a little low in my emergency fund, and that I should bolster it when I have the opportunity.

Where Personal Capital excels in easily providing you with your information, Mint excels in functionality. In addition to showing you all the same information as Personal Capital, Mint supplies your credit score, and allows you to pay bills right from within the app itself. It’s also a little more modern and clean than the Personal Capital app.

Both are really great apps. I personally use Personal Capital, but I’ve used Mint and love them both. Either would help you keep better track of your personal finances and be a little smarter with your money. And they’re both free to use!

Best Apps to Make Some Extra Money

If you’re looking to make some extra cash, there are a lot of apps that can help you do just that. Below are some popular cash-generating apps perfect for college students.

Blast and MISTPLAY

Blast is an app that literally pays users to play games on their phone. What could be better than that?

It works like this: Blast recommends games for you to play. When you complete certain missions in those games (for example, reaching a certain level or playing for a certain length of time) you will earn money and experience points. The money is deposited in an FDIC-insured savings account that earns an interest rate of 2%; the experience points help you rank on the Leaderboard, where you can earn even more money.

Most missions pay out somewhere between 25 cents and $1.25, but there are some that can go even higher than that. Bear in mind, you’re not going to get rich by playing games on Blast. But if you already play games on your phone in between classes or while you’re on the bus, using Blast is a great way to get paid for something that you’re already doing.

MISTPLAY works in a similar way to Blast, allowing you to make money by playing games. By downloading and playing games recommended to you through the MISTPLAY app, you’ll earn “Units,” which are essentially points that you can redeem through the app. These points can be used to upgrade your avatar, or they can be redeemed for gift cards from companies like Amazon, Google Play, XBox, iTunes, Starbucks, and Visa.

Units don’t translate well into a straightforward dollar amount, because the exact value of your Units will depend on what you redeem them for. Gift cards with a higher face value are technically cheaper that those with lower face values, which encourages users to save up their points. That being said, you can typically redeem your Units using the exchange rate below:

- $0.50 for 400 Units

- $5.00 for 1,800 Units

- $10.00 for 3,000 Units

- $15.00 for 4,500 Units

- $25.00 for 7,500 Units

- $50.00 for 15,000 Units

Of the two, I personally prefer Blast because it’s so simple to use. There’s no exchange rate to worry about or minimum amount that you need to earn before you can transfer your funds out of your Blast account; once you earn the money, it’s yours to use as you wish. That being said, both apps allow you to make money playing games in your spare time. Ultimately, when choosing between the two it will just depend on your preference.

Sweatcoin

As a college student living on campus, you probably spend a whole lot of time walking. Walking between classes, walking to the library, walking to the dining hall, your on-campus job, your dorm, etc. Sweatcoin is an app that pays you for walking.

Designed to encourage its users to get active and stay fit, Sweatcoin turns your smartphone into a pedometer, allowing the app to (roughly) count your steps. For every 1,000 steps you walk, you earn 0.95 sweatcoins, a digital currency which you can then redeem for rewards (often fitness inspired items like headphones, water bottles, yoga equipment, etc.) or gift cards.

If you’re someone who walks a lot—whether a college student, someone living in a walkable city, an athlete, or someone with a job that keeps you on your feet—Sweatcoin can help you earn a little extra cash for doing something that you have to do anyway.

Leveraging Technology to Crush Your Financial Goals

With all these great tools at our disposal, we would be fools to not put them to good use. Choosing just one or two apps from each of the categories above means that you’ll be laying the groundwork to hit your goals, whatever they are.