When it comes to paying back your student loans, there are many different strategies that you might consider to make the process simpler, easier, and less complicated. One popular option that many borrowers of federal student loans turn to is a process known as student loan consolidation.

Are you considering student loan consolidation? Below, we explain what consolidation is, what the process looks like, and answer common questions that borrowers often have about consolidation so that you will be able to make a more informed decision about whether or not consolidation is right for you.

Contents:

- What is student loan consolidation?

- How to Consolidate Federal Student Loans

- How to Consolidate Private Student Loans

- Student Loan Consolidation FAQs

What is student loan consolidation?

Student loan consolidation is a specific process that borrowers can use to take multiple federal student loans and combine them into a single, new federal student loan. The resulting loan is called a Direct Consolidation Loan.

This new loan will carry an interest rate equal to the weighted average of all of the loans that you’ve consolidated. In other words, consolidation really won’t make your loans any cheaper because your interest rate doesn’t change, but if you have many loans it could make repayment simpler.

Depending on your needs and goals, you can choose to consolidate all of your federal student loans, some of them, or even just two, while leaving the others as is.

How to Consolidate Federal Student Loans

1. Keep track of your student loans.

Before you begin the consolidation request, it’s important that you have a complete list of all of your student loans and as much information about those loans as possible. At a minimum, this list should include the loan number, the loan’s balance, the interest rate, and whether it is federal or private.

Next, split your student loans into two groups: One for federal student loans and one for private student loans. This is important because consolidation only applies to federal student loans.

A student loan spreadsheet can be an easy and effective way of keeping track of your student loans and organizing all of the loan information.

Download our free student loan spreadsheet here.

2. Gather all of the required information.

To make the consolidation request process easier, you will want to gather all of the required information ahead of time, before you start. You will need:

- A verified FSA ID

- Personal information: Including your permanent address, email address, phone number, and the best time to reach you

- Financial information (optional)

If you will be applying for an income-driven repayment plan, then you will also need to provide financial information. The consolidation request system includes a tool which has the ability to pull your most recent tax information from the IRS. This makes it easy to provide your financial information. If your income has changed since you last filed taxes, you can also opt to deliver certain statements directly to your servicer instead.

3. Visit Studentloans.gov and log in.

Then click the button to begin the consolidation process. This will launch a dashboard that displays your federal student loans and guides you through the consolidation process. You will need to complete the application in a single sitting, which is estimated to take approximately 30 minutes from start to finish.

4. Choose which loans you wish to consolidate.

The dashboard will display all of the federal student loans on record in your profile. Review this information for accuracy. If any loans are missing, there is a button you can press to add those missing loans.

Then, you will need to select which loans you want to consolidate. Remember that if you are working toward student loan forgiveness (for example, on a Perkins Loan) that consolidation will remove your eligibility for forgiveness. If this is important to you, you can choose to consolidate only those loans which you are not seeking to have forgiven.

The dashboard will automatically display the new loan amount and the new weighted interest rate, so you can immediately see what your new consolidation loan will look like.

5. Choose a grace period.

If one or more of the student loans you are consolidating is currently in a grace period, you can choose to delay processing your consolidation request. This is completely up to you. If you would prefer to process the request immediately, that’s fine too.

6. Choose a new student loan servicer.

If you would like to keep your student loans with your current student loan servicer, then you should choose them from the list. If, however, you would prefer a new servicer, now is your opportunity to make that selection.

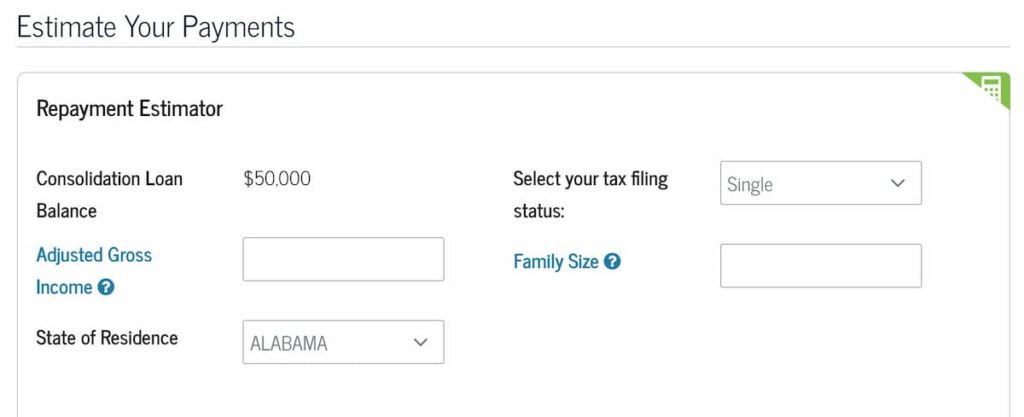

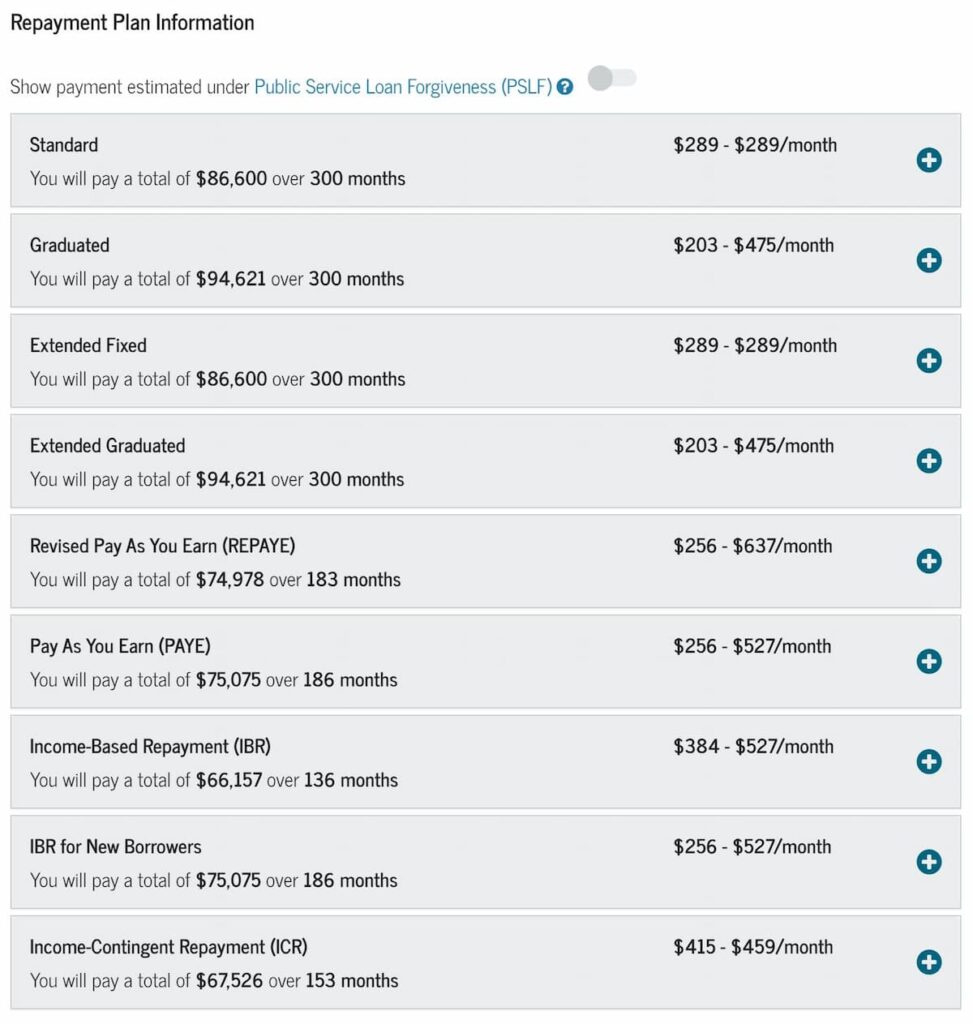

7. Choose a repayment plan.

On the next screen, you will be asked to enter your adjusted gross income, state of residence, tax filing status, and family size. This will allow you to estimate your monthly payment size.

Further down on this page, you will see a full list of all of the different repayment plans that you can choose from. This chart will include your estimated monthly payment, how long you will be in repayment, and the total amount that you can expect to pay. Select the repayment plan that is most appealing to you.

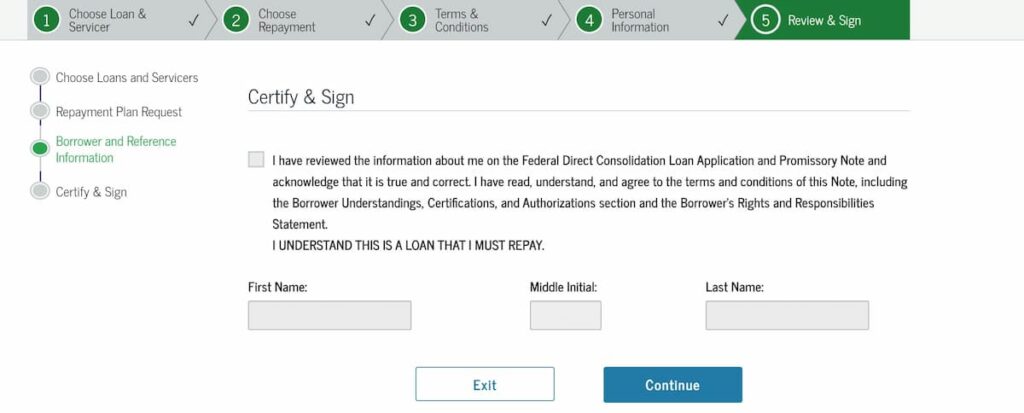

8. Review the terms of your new loan.

Before you submit the form, it’s essential that you understand the terms that you are agreeing to. After all, this is a binding legal document, and you should never sign such forms without due consideration. Once you are sure you understand the terms of the new loan, you can either submit the form to officially request consolidation or you can simply close out the window to stop the process.

9. Continue making payments as usual.

It may take a few weeks for your loans to successfully consolidate, at which point your student loan servicer will contact you. You should continue to make all regularly scheduled payments on time and in full while you await confirmation that the consolidation is complete. Failing to make payments will reflect poorly on you and could cause issues with the consolidation process.

10. Talk to your servicer.

If at any time you are unsure of something or you have questions about the consolidation process, you should reach out to your student loan servicer. After all, it is their job to help you repay your student loans, and a key part of that is ensuring that you understand your options when it comes to consolidation.

How to Consolidate Private Student Loans

Do you have multiple private student loans that you would like to consolidate into a single new loan? Or do you have a mix of both private and federal student loans and a hope to make repayment simpler by merging them together?

The only way to do this is to go through a process known as student loan refinancing. While refinancing is similar to consolidation in a number of ways, it is also very different, and it’s important to understand these differences before you decide to move forward with refinancing.

For example, while student loan consolidation will never result in you saving money (because it doesn’t change your interest rate), refinancing could save you money if your new loan has a lower rate. But, if you refinance federal student loans you effectively convert them into private student loans, which means that you will be giving up key protections and benefits like income-driven repayment plans, the ability to place your loans into deferment or forbearance, student loan forgiveness options, and more.

You can learn more about student loan refinancing here.

Student Loan Consolidation FAQs

1. Why consolidate your student loans?

The primary reason that people choose to consolidate their student loans is because they want to make repayment simpler. This is especially the case when you have many different federal student loans with different payment due dates and even potentially held by different servicers. By consolidating into a single new loan, you will only have one payment due date to remember and one payment to make, which can admittedly make it easier to stay on top of your debt.

Another reason people choose to consolidate their loans is that it gives you the opportunity to take older variable-rate federal loans and consolidate them into a new loan with a fixed interest rate. This makes it easier to know exactly what your payments will be at all times, which can offer some peace of mind compared to variable-rate loans.

When you consolidate, you can choose to extend your repayment term up to 30 years. Doing so will lower your monthly payment amounts, making it easier to make payments, but will ultimately increase the amount that you pay in interest over the life of the loan.

Finally, consolidating your loans may open some forgiveness options and income-driven repayment plans that were otherwise not available to you under your original loans. This will depend on the type of loans that you originally carry.

2. What are the pros and cons of student loan consolidation?

There are a number of pros and cons of student loan consolidation that you should understand before making a decision either way.

Pros of Student Loan Consolidation

- Consolidation can make repaying your student loans less confusing.

- Consolidation can lower your monthly payment.

- Consolidation may give you access to important benefits.

- Consolidation can convert variable-rate loans into fixed-rate loans.

- Consolidation gives you more options for deferment.

- Consolidation can help you avoid default.

Cons of Student Loan Consolidation

- Consolidation might increase your total interest payments since it lengthens your repayment term.

- Consolidation may add to your principal.

- Consolidation might cause you to lose certain benefits.

- Consolidation will reset the clock on student loan forgiveness.

- Consolidation won’t lower the interest rate on your student loans.

- You can’t consolidate your private student loans.

- If you consolidate, you can’t pay off loans with higher interest rates first.

3. Can you consolidate private student loans?

As mentioned above, no, you cannot consolidate private student loans into federal student loans. The only way that you can merge together multiple private student loans into a single new loan is through a process known as student loan refinancing.

4. Should you consolidate your student loans?

Ultimately, only you can answer this question.

If you are overwhelmed by the sheer volume of federal student loans that you have, need to lower your monthly payment, want to convert variable-rate loans into fixed-rate loans, or need to avoid defaulting on your loans, then consolidation can help you achieve this.

If, however, you have made significant progress toward student loan forgiveness, you might want to reconsider consolidation, as this will reset the clock toward forgiveness.

Meanwhile, if you would like to lower your interest rates and are okay with the idea of giving up the benefits that come with federal student loans, you might want to consider refinancing your student loans with a private borrower instead.