If you’re a college student, chances are good that you don’t think about your finances too often. Between studying for exams, making sure you get the a decent roommate next year, and navigating the tricky world of college romance, your plate is pretty full.

And when you do think about money, it’s either to figure out whether you have enough in your checking account for a cheap 30-pack of beer for the weekend, or it’s to have an existential crisis about the massive amounts of student loans you’ve racked up (which you’ll soon need to pay back).

If you’re particularly finance-focused, you’re asking questions like:

- Should I pay my student loans off early?

- How do I pay my student loans off faster?

- Can I pay my student loans early?

And then here I come, telling you that on top of everything else, you should be investing while you’re in college. Yeah, right.

But hear me out.

One of the biggest advantages that college students have over their older siblings, parents, and grandparents is time. Time is an incredibly powerful thing, especially when you’re talking about money and investing. And the sooner you start, the more powerful it becomes.

Investing in College

Okay, I know you’ve heard the term “compounding” before. Usually it’s used to talk about savings accounts and the interest that they earn, but it also applied to your investments.

Want to learn the basics of investing? Check out our guide to the essential investment terms and definitions for beginners!

Compounding essentially means that your money is making money. In terms of a savings account, it is when the interest that you’ve accrued begins to accrue its own interest, on top of the principal. In terms of investments, it’s when your investment profit begins to generate its own profit, on top of what the principal generates. (Quick side note: Interest Capitalization is the exact opposite of compounding, and something that you should avoid.)

Compounding works over time to turn an initial investment into a much more substantial investment. The longer you are able to keep your money invested, the more profit it can generate for you. Every year that you put off starting is a year that you’re missing out on the magic of compounding, and it really adds up over the years. In fact, waiting just 4 years to start investing could mean a difference of nearly $50,000.

Don’t believe me? Take a look at the hypothetical below.

Here, I’m using the Dave Ramsay Investment Calculator to illustrate investment returns. It’s a great tool that you should check out if you’re really interested in starting to invest.

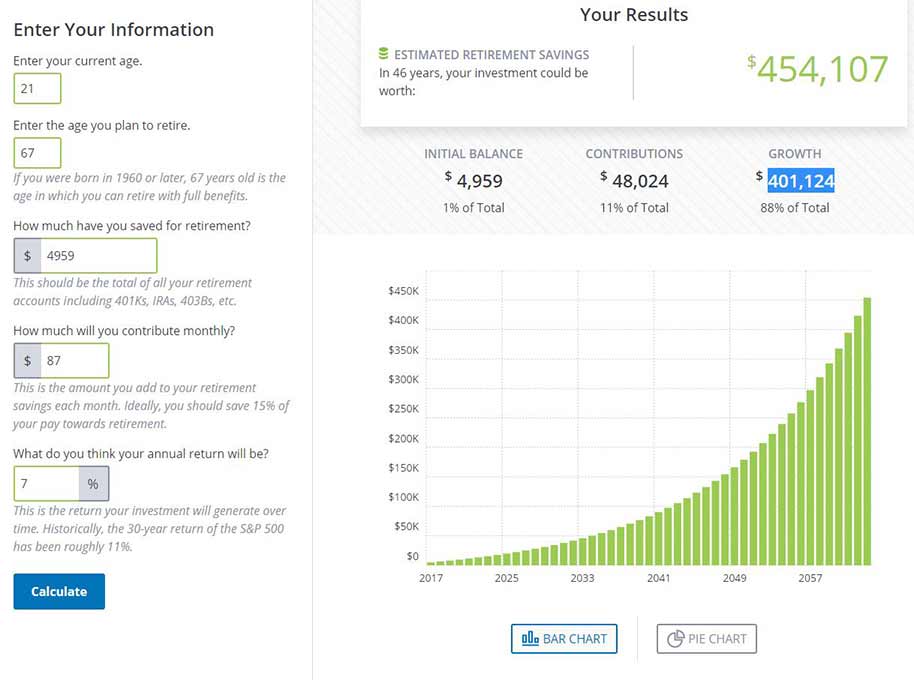

Let’s say that you start investing as a freshman in college, when you’re around 17 years old. You don’t have a lot of money, cause you’re also using your work study to pay down your debt while you’re a student (smart!). But you’re able to save $20 each week, which you decide to invest. That’s equal to $1,040 a year, or about $87 a month. Assuming a (very modest, but reasonable) average return of 7% annually, when you graduate at 21 you’ll have about $4,959 dollars invested ($783 of which is profit). Very nice!

Now let’s say that you keep that money invested, and continue to invest $20 a week ($87 a month) into your account until you retire. Again, assuming a modest 7% average annual return and a retirement age of 67, when you retire your investment would grow to a whopping $454,107, and $401,124 of it would be pure investment profit. All of that, for just $20 a week!

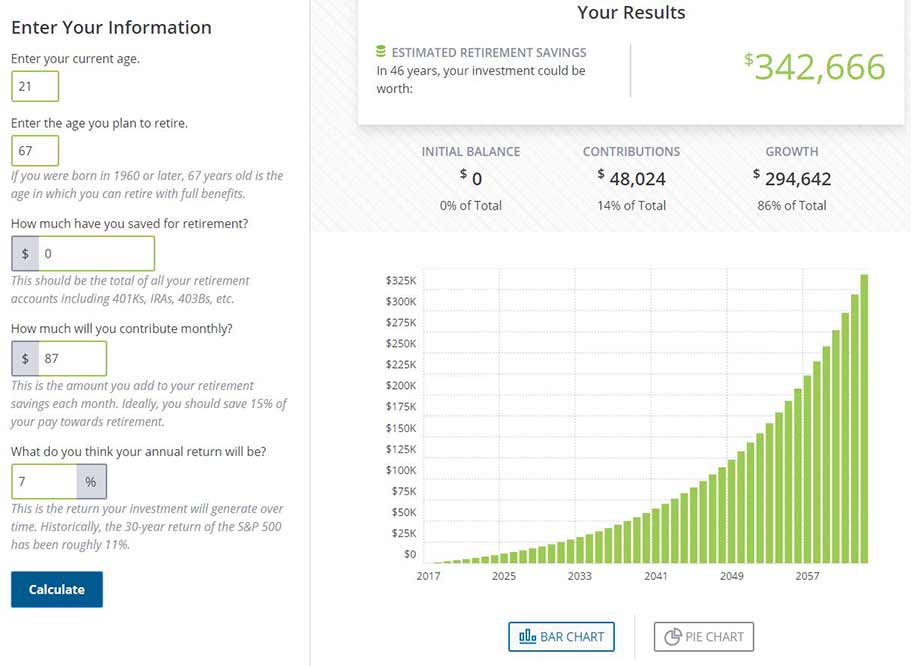

But now, let’s say that instead of investing those $20 a week while you were in college, you spent it on bad beer and greasy pizza. Instead, you started investing after you graduated, at 21 years old, and contributed $20 bucks a week ($87 per month). Earning the same 7% average annual return, your account would be worth $342,666 when you retire at 67, of which $294,642 is investment profit. That’s more than $100,000 less than you would have if you started to invest while you were a college freshman! (It’s $111,441 less, to be exact.)

That’s absolutely insane. It’s the magic of compounding at work. It’s why college students need to start investing while they’re still in school.

So should I start investing or pay off my student loans first?

I now what you’re thinking. “Wait a minute,” you say into your computer/phone/tablet screen. “Isn’t this website focused on helping college students pay off their student loans? Shouldn’t you be telling me to prioritize paying off my college debt over everything else?”

Yes, most of the content on this website will tell you about the benefits of paying off your student loans. And yes, depending on your own financial situation and goals, paying down your debt before you begin investing might be the best option for you. But it bears saying: You don’t need to be free of debt in order to start investing. Actually, waiting until you have fully paid off all of your debt before you start investing your money could be a recipe for disaster.

Why? Two reasons.

1. Yes, paying off your student loans early has the potential to save you thousands of dollars in interest compared to following a typical 10-year repayment plan. And yes, paying off your debt will probably do wonders for your psychological well being. Heck, that’s why I recommend it, why I’m striving to pay off my loans early, and why I started this website.

BUT, and this is a big but: The amount of money you save by paying your loans off early likely won’t be anywhere near the amount of money you stand to make by getting started with investing early.

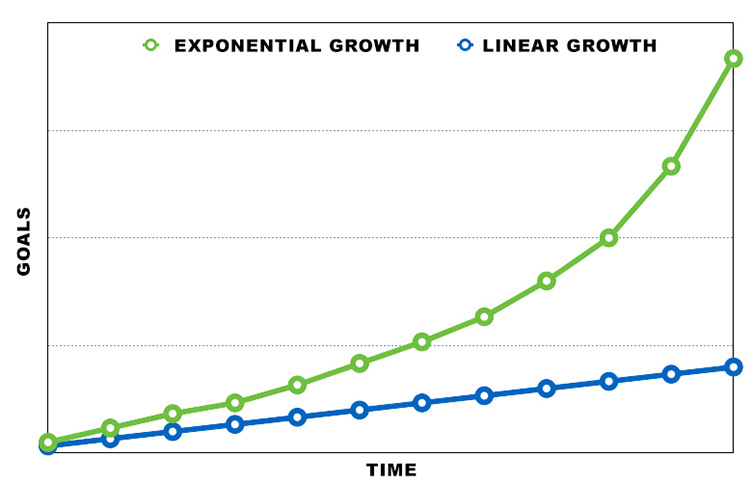

Debt repayment offers linear return on your money, whereas smart investments have the potential to offer exponential growth. (Just in case you flunked out of calculus, the quick and dirty chart below illustrates why exponential growth is better.)

What makes investing so special compared to debt repayment? Again, it’s all about the magic of compounding. Once your investment profit starts making its own profit, you’re on your way towards exponential growth.

Investment Fact: From 1928 to 2014, the S&P 500 gained an average yearly return of 9.8%.

2. You will most likely always have some form of debt holding you back. If it isn’t your student loans, then it’s your car loan or your mortgage. Waiting to start investing until you have paid off all of those debts means that you won’t start investing until your 40s, or 50s, or 60s, and by that point you’ll have lost the amazing benefit of time that you have right now. That all adds up to a pretty dreary retirement where you’re going to have to subsist on Social Security.

The truth is, you shouldn’t be paying off your student loans or investing for the future. You should be doing both. At the same time. Paying down your college debt and investing. And the sooner you can start on both, the better off you’ll be. (One Note: If you have substantial credit card debt, focus on paying that down as soon as possible. Interest rates on credit cards easily tops any investment gains you might make, so you should definitely focus on paying off your credit card debt before you start investing).

College students should be doing everything in their power to reduce their college expenses and begin paying down their student loans while they’re still in school, because this will limit the number of student loans that they’ll need, amount of interest that they’ll pay over the life of their loans. But they must begin investing as soon as possible to capitalize on their youth. It’s as simple as that.

I foolishly didn’t begin investing until long after I graduated. Had I started investing when I was still a college student, back in 2008–09, I would have lost a bit of money in the short term because of the recession. But in the long term, I would have more than tripled my money between then and now. I’m still kicking myself for that lapse in judgement.

How College Students Can Start Investing

There are tons and tons of ways that you can start investing money in the stock market. But before we dive into specific investment methods, I want to start by making one statement up front: You need to make sure that you’re investing in a diversified, balanced portfolio. This means that you aren’t just invested in one company or in one industry, but in a number of companies. Ideally, all of them.

Why? Because it is incredibly difficult to “win” at investing when you’re buying individual stocks. And if that one company or industry performs badly, then you stand to lose a good chunk of change.

Instead, especially when you are first getting started, you should be looking to invest in the broad market. This means investing in ETFs (Exchange traded Funds), which mirror large chunks of the market or whole indexes (like the S&P 500, the Dow Jones, or the Nasdaq). By investing in the broad market, when the market gains value, you’ll make money. If you go back and look at any of the major indexes, what you’ll see is that the stock market is incredibly volatile, but it has always trended up over the long term. Yeah, picking a superstar stock like Netflix or Amazon and getting in on the ground level might make you a lot more money, but it is insanely difficult to do. Investing in the broad market and doing so consistently and regularly over time is a much safer way of building wealth.

Before you even begin considering how you want to invest, you need to be able to answer the question why? Why do you want to invest, and what are your investment goals? These are critical questions for you to be able to answer, because they will impact your investment strategy.

Are you investing for retirement? If so, you’ll want to look into tax-advantaged investment accounts like an IRA or 401k. You’ll also want to consider being more aggressive in your investments, since you have so much more time to make up for any losses. Are you investing for the long-term (20+ years), but not for retirement? That removes IRAs and 401ks from your consideration, but you would still probably want to be more aggressive in your allocation. Are you investing for the medium-term (5–10 years), such as to buy a house? Then you’ll want to be a bit more conservative in your asset allocation. Are you investing for the short term (3–5 years)? Then you’ll want to bee the most conservative in your investments.

Once you know your investment goals and timeline, you can then begin considering your specific options (below).

1. Open a retirement account (IRA, 401k, 403b).

If you’ve decided that you are specifically going to invest for retirement, then you should very strongly consider opening a retirement account so that you can benefit from some of the tax advantages that they come with.

Long story short, the government wants you to start investing for retirement. To help give you incentive to get started, they created tax breaks that make investing seem more worthwhile. Depending on the type of retirement account that you have, you either get your tax break up front (you don’t pay taxes on the money that you invest until you withdraw from your account in retirement), or you get your tax break in retirement (you pay taxes on the money that you invest before it is invested, but then don’t pay income taxes on it when you withdraw in retirement).

The main types of retirement accounts available to individuals are:

- Individual Retirement Accounts (IRAs): An IRA is a retirement account that anyone can open, whether they have an employer or are self-employed. They come in two flavors: Traditional IRA and Roth IRA. If you have a traditional IRA, then you do not pay taxes on the money you invest until you withdraw it during retirement. If you have a Roth IRA, then you pay taxes on the money you invest up front, and then do not pay taxes on t during retirement. In 2017, individuals could contribute up to $5,500 each year into an IRA account (up to $6,500 if you are over 50 years old).

- 401k: A 401k is a retirement account specifically sponsored by your employer. You can only invest in a 401k if you have an employer that has access to a plan. Like IRAs, they can be either a traditional 401k (taxed in retirement) or a Roth 401k (taxed up front). In 2017, individuals could contribute up to $18,000 each year into a 401k account (up to $24,000 if you are over 50 years old).

- 403b: A 403b is essentially a 401k, but for public school teachers, non-profit workers, and employees of certain other sectors. They work the same way as 401ks, with the same contribution limits. You can have either a Roth 403b or a traditional 403b.

The tax breaks are the largest benefits of opening a retirement account. Unfortunately, though, there are certain cons that you should consider:

- Since you’re a college student, you likely do not have access to a 401k or 403b. This means that you are limited to contributing only $5,500 a year to your retirement account. Since you probably have limited funds, that might be fine for you, but if you do happen to have more money that you want to invest, you will need to look into opening another kind of account on top of your IRA.

- If something happens and you decide that you need to withdraw money from your retirement account before you reach retirement age, you will be hit with taxes and penalty fees that will really drive down the value of your account. (Wells Fargo has a calculator you can use to see what these fees might look like.) That’s why it’s important that you build an emergency fund before you begin investing, so that you aren’t tempted to cash out your investments when an unexpected expense pops up.

2. Open a do-it-yourself brokerage account.

If you aren’t investing for retirement, then you will probably want to think about opening a do-it-yourself brokerage account through a service like Ally, E*Trade, or Ameritrade. (Reviews.com has a great review of the top 5 online stock trading sites, which you should check out if you’re looking to go this route.) Doing so means that you’ll be completely 100% responsible for creating your own portfolio and making sure that your asset allocations match your investment timeline, goals, and risk tolerance.

The main benefits of building your own portfolio instead of turning to a broker or investment adviser are that:

- You do not have to pay anyone a fee just to manage your account.

- You have complete control over your investments, allowing you to choose very specifically the types of companies you invest in.

- Exchange Traded Funds (ETFs) make it much easier to build a balanced portfolio than it used to be.

- Choosing a winning investment on your own and watching it grow in value is a reaaaaaally good feeling.

There are, of course, a lot of potential downsides that you need to consider:

- Though you won’t pay management fees, you will pay a fee each and every time you make a trade (this means every time you buy or sell). Fees depend on the service that you use, but Scottrade, for example, charges $7 per trade. Especially for college students, who might be investing as little as $20 a week or month, paying $7 in fees is a huge percentage.

- Building a portfolio from scratch is confusing, and that’s a big reason people think investing is too hard for them. It takes a lot of time and patience to figure out what your portfolio should look like, and it is, frankly, intimidating.

- Having complete control comes at the expense of not having experts to rely on for feedback. It also means owning up to your mistakes. Though choosing a winning investment and watching it grow feels amazing, choosing a losing investment and watching it tank can be downright devastating.

3. Find an app to help you get started.

If you are a college student who doesn’t want to invest for retirement, doesn’t want to pay management fees to a broker, and doesn’t have the time or wisdom to build your own portfolio, do you have any options left that can help you get started investing? Yes! And it’s likely already in the palm of your hand: Your phone.

Today’s young investors have it better than ever before, all thanks to technology, which has flooded the marketplace with services and apps that make literally every aspect of life easier. And that goes for investing as much as it does for anything else. There are all sorts of investing apps that are designed explicitly for new investors.

My favorite investing app, especially for college investors, is Acorns. It’s an app that I personally use, and that I recommend to literally all of my family, friends, dates, and strangers. Why? For a few reasons:

- If you are new to investing, you do not need to worry about building your own portfolio from scratch. You simply select a portfolio designed by the company, based on your investment goals and risk tolerance. The app even has a short quiz to help you decide which of the five portfolios best matches your needs.

- Investing through Acorns means you are investing predominantly in exchange-traded funds (ETFs) which means you’ll instantly have a pretty diversified portfolio without needing to think about individual trades.

- There are no fees that you pay per trade. You are charged a $1 a month maintenance fee for a simple investment account, $2 per month to add an IRA, and $3 a month to add on a debit card. Plus, college students with a valid .edu email address pay NO FEES for 4 years from registration, which means you have 4 years to grow your money for free.

- There is no minimum account balance or minimum investment necessary, making this a great tool for college students who have a tight budget. You can invest as little as $5 at a time. Other investment apps usually require a minimum opening investment that can be hundreds or thousands of dollars.

- Being app-based, you always have access to your investments.

- The app offers multiple ways to invest and save, from using their “round-up” system to setting up a recurring investment to referring friends to “finding money” by shopping with certain brands.

- Acorns wants you to learn. That’s why the app has a knowledge center that links it to their online magazine, Grow, which aims to teach readers about all things investing and personal finance. (Also a positive: I write for them occasionally, meaning you get more of me!)

Sounds great, right? If you’re interested I encourage you to learn more about them and try them out.

I personally use Acorns as my primary investment portfolio (I’m in the aggressive portfolio) and I love it. That being said, it isn’t for everyone. I also use the Stash investment app, which I really like because it offers a lot of different “Themes” that I can decide to invest in. You can read my full review of Stash here, if you’d like to learn more.

Regardless of who you use, you just need to make sure that you have a diversified portfolio that you are regularly contributing to over time, and that doesn’t charge outrageous management or trading fees.

Other investing apps that you can use to dip your toes in the water, and which I’ve used in the past, include things like Betterment, Robinhood, and Stash, all of which have their own unique perks.

The Bottom Line

Student loans suck—believe me, I know. That’s why I’m working hard to pay mine off, and why I think everyone should pay them off as fast as possible (or avoid them altogether). But if you are thinking that you need to pay off your student loans before you can start investing for the future, you’re wrong. The truth of the matter is, you should be doing both in order to improve your current financial situation (by paying off your debt) while building up a comfortable future (by investing).

College students have the amazing gift of time on their side, making a smart approach to investing all the more important. Don’t give up that gift, or you’ll regret it.

Note: This was a very, very quick introduction to the concept of investing, and is not meant to be the sole resource you use to create an investment strategy. I highly recommend you background yourself a bit more before getting started. If you’re looking for some websites and blogs that you should start reading before diving into the investment waters, I recommend you take a look at our roundup of the Best Personal Finance Websites for College Students.

Looking for other helpful tools that can help you get your finances on track? Check out this list of amazing personal finance apps that can help you do everything from start investing to saving to paying down your debt and more!