Okay, so my opinion on student loans is no secret: Student loans suck. That’s why I built this website, after all. But the truth is, student loans are an essential part of many people’s lives. Without them, a college education could be out of reach for millions of students every year, often making them a necessary evil.

If you’re brand-new to the world of student loans, you should take a look at our introductory guide that will help you understand all of the student loan basics.

Are you trying to decide if taking out student loans to pay for school makes sense for you? Are you wondering if the cost of student loans are worth it in the long run? The answer to those questions is highly dependent on each person asking them; the answer won’t be the same from me to you or from you to your siblings or friends. All you can do is weigh the positives and negatives, the advantages and disadvantages, and make the decision that seems best for your own personal situation.

Need help keeping track of your student loans? Download our free Student Loan Spreadsheet!

With that in mind, I wanted to compile a list of all the major pros and cons of taking out student loans to pay for college. If you are applying for colleges and are considering taking out student loans to afford your education, keep these student loan benefits and drawbacks in mind before making a decision either way.

Pros and Cons of Student Loans

| Pros of Student Loans | Cons of Student Loans |

|---|---|

| 1. Student loans let you afford college. | 1. Student loans can be expensive. |

| 2. Student loans can mean the difference between an okay school and your dream school. | 2. Student loans mean you start out life with debt. |

| 3. Student loans can be used for things besides tuition, room, and board. | 3. Paying off student loans means putting off other life goals. |

| 4. Paying off student loans will help you build credit. | 4. It's almost impossible to get rid of student loans if you can't pay. |

| 5. Defaulting on your student loans can tank your credit score. |

Pros of Student Loans

I know, the words “pro” and “student loans” don’t seem like they should ever be used together in the same sentence. But I promise you, there are at least a few. Otherwise, no one would ever take out student loans!

1. Student loans let you afford college.

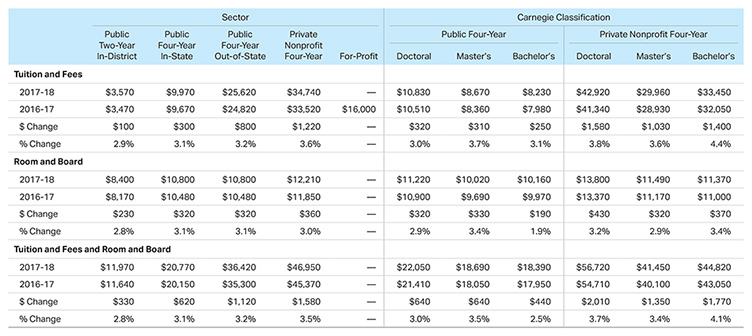

The average cost of college tuition, room, and board for the 2017–18 academic year is between $20,770 (4-year, public, in-state) and $46,950 (4-year, private), according to College Board. How many college students or recent high school graduates do you know that can afford between $80,000 and $188,000 for four years of college? Even when you lump in help from parents, it’s a small percentage of Americans that can afford a price tag like that without taking out any student loans at all.

The simple fact is, college is so expensive that for the vast majority of Americans, it would be nearly impossible to afford without the help of student loans. I would definitely say that something that allows you to follow the American Dream and earn a quality education can’t be all bad.

2. Student loans can mean the difference between an okay school and your dream school.

Look at the chart above, and notice the huge difference in price between a public 4-year college and a private 4-year college. The private college costs more than double what the public university does.

Now imagine that your parents did their best over the years to sock away money over the years for your education, and they were able to save enough to cover four years at a public university. If the public university offers the courses you want to take and fits into your plan, then great: You can graduate from college debt-free!

But what if it has always been your dream to go to Yale, or some other private school. You’re accepted, but your parents weren’t able to save enough money to cover all of it. You’d be stuck still having to cover $20,000 though other means, most likely a mix of financial aid and student loans. If you didn’t have access to student loans, you would be forced to go to the college that you could afford out of pocket. But because student loans exist, you have the ability to decide: Go to the okay school and graduate debt-free, or go to your dream school and take out student loans to pay for it.

The decision you make is, ultimately, your own, and whether or not going to the more expensive school is the better decision will depend on your own financial situation. That being said, the fact that student loans offer the ability to choose is definitely a positive.

3. Student loans can be used for things besides tuition, room, and board.

Many people think of student loans as only being able to be used on things like tuition, room, and board. And though it’s true that that is what you will use the bulk of your loan money on, you can also use your funds for essential college expenses like textbooks, a laptop, and computer software. Those are not insignificant costs, and the fact that student loans can ease the burden on you and your family is a good thing. However much student loans suck, they carry much lower interest rates than expensive credit cards or personal loans.

That being said, when it comes to using your student loan funds, you should of course be smart with how you spend it. Only buy what is necessary for your education. No splurging! By keeping your college expenses as low as possible, you’ll be able to take out fewer student loans. And that means more money in your pocket once you graduate.

4. Paying off student loans will help you build credit.

Yes, that’s right: Student loans, used responsibly, can help college students and graduates build their credit scores. In fact, because many college students don’t have any other bills or debts associated with their names, student loans may be the only way for students to begin building their credit history. Having a good to excellent credit score will come in handy throughout the rest of your life as you apply for apartments, look for credit cards, finance a home purchase, and even when you’re applying for jobs.

But to realize these awesome benefits, you’ve got to make sure you’re using student loans responsibly. Only take out as much as you know you can repay, try making interest-only (or more!) payments while in school to keep your balance low, and make sure that you always—always!—make your monthly payments.

Cons of Student Loans

1. Student loans can be expensive.

When you borrow student loans to pay for your college education, you don’t just have to pay back the amount that you borrowed: You have to pay back interest as well. This can range anywhere from 4.45–7% for federal student loans (in 2018) to a high of 11–15% for private student loans. On the high end, that can be comparable to a credit card. If you can afford to pay for college without using student loans, it would definitely be in your best interest to do so. And be sure to always accept federal student loans first, before turning to private student loan companies, to save the most money. Follow this order when accepting your student loans to graduate as cheaply as possible.

2. Student loans mean you start out life with debt.

If you rely on student loans to pay for college, that means that you will start out your adult life in debt. Sure, that college education might mean that you earn more money over your lifetime than someone with only a high school diploma. But, depending on how much you borrow, it could mean for a difficult first few years out of college, especially if, like millions of other college graduates, you’re having a hard time finding a job that pays enough money to allow you to live a decent life. (Luckily, if you’re having a hard time making payments on your federal student loans, you have options.)

Taking out fewer (or no) student loans could mean the difference of being able to live a comfortable life and struggling just to make ends meet. Take it from me, it’s no fun living in your mother’s basement until you’re 28 years old.

3. Paying off student loans means putting off other life goals.

The average monthly student loan payment in 2018 is $351. But many college graduates find themselves paying higher amounts, especially those who had to take out private student loans. (I personally pay $611 every month to cover my student loans, and that’s without factoring in the extra payments I make to pay them off faster.) That’s money that you could be using to save for a down payment on a house, finance a wedding, or invest for your long-term financial goals. If you’ve got a substantial amount of student loan debt, you might not be able to start pursuing these other financial goals until after you’ve finished paying off your debt, and at that point you’ll have to double your efforts to make up for lost time. No bueno.

4. It’s almost impossible to get rid of student loans if you can’t pay.

If you can’t afford to pay your mortgage, your credit card bills, your car loans, or your medical bills, it might seem like your world is coming to an end. But you’ve got one final emergency valve you can release in those situations which can allow you to dig your way out of debt: You can declare bankruptcy.

Editor’s Note: Declaring bankruptcy is by no means something to take lightly. Yes, it has the potential of drastically reducing the amount of money you owe on your debts, but it will also cause your credit score to plummet for nearly a decade after the process is done. It’s there for emergencies.

Unfortunately, declaring bankruptcy will very rarely get rid of your student loans. Under current law, they’re nearly impossible (but not entirely impossible) to discharge in bankruptcy, and that’s a big deal for people who find themselves unable to pay for whatever reason. Imagine not having health insurance, being diagnosed with cancer, taking on medical debt to afford chemotherapy in order to live, and then needing to declare bankruptcy because you can’t afford your hospital bills. And then, on top of that, still having to pay your student loans.

Luckily, there are some other ways of getting rid of student loan debt through discharge and forgiveness.

5. Defaulting on your student loans can tank your credit score.

I mentioned above that responsibly using student loans can help you build a credit history and, with it, a credit score that will be useful throughout your life. But the alternative also holds true: If you are irresponsible with your student loan use, you can cause significant damage to your credit score.

What does irresponsible use of student loans look like? Taking out more than you can expect to pay off after graduation, failing to make your monthly payments on time, and defaulting on your student loans can all have major negative consequences for your credit score. Defaulting is the worst of all outcomes, as it means that you’ve gone for more than 270 days without making a payment on your student loan.

A bad credit score can follow you throughout your life, making you pay more for everything from credit cards to car loans to mortgages. It could even cost you your job.

Luckily, if you find yourself unable to make your student loan payments, you have options available to you. Income-based repayment plans can help you find a payment amount that fits into your monthly budget; deferment and forbearance can see you through periods of economic hardship, and the Department of Education has even set up a default rehabilitation program to help you recover from default without damaging your credit score. If you can’t make your payments, you need to communicate to your lender.

A Necessary Evil

I can honestly say that there is nothing inherently bad or wrong with the concept of student loans. People borrow money to pay for things that they need all the time. Car loans, mortgages, college—think of all the significant things that you might not be able to afford without relying on debt. Would you be better off if you could pay for these things yourself so that you don’t need to pay interest on top of what you borrowed? Of course. But for many Americans that just isn’t an option.

Student loans, used properly, can make a lot of sense and can be used for a lot of good. The real issue isn’t the concept of student loans, but the reality: High interest rates, laws that make it near impossible to discharge college debt even in bankruptcy, astronomical college prices that each year pull the dream of a college education out of reach of millions of Americans. That’s why it’s so important that if you do decide to take out student loans, you limit the amount you borrow as much as possible and then pay them off as quickly as possible once you graduate.

Are you looking for ways to pay back your student loans? These articles can help:

- Pay Off Your Student Loans

- How to Keep Track of Your Student Loans

- Pay Off Your Student Loans Faster With These 6 Strategies

- 3 Great Strategies for Paying Off Student Loans Faster

- Why You Should Use Your Tax Refund to Pay Down Your Student Loan

- Student Loan Refinancing Guide

- 9 Pros and Cons of Refinancing Your Student Loans

- 13 Pros and Cons of Consolidating Student Loans

- Starve & Stack Method for Student Loans

Great post.

Thanks! you helped me with my BPA project.

I am surprised that the student loan lenders haven’t yet applied the “Rule of 78s” to student loan contracts. This type of prepayment penalty disguised as a “rebate” could block force all of the interest over the life of the loan onto the principal amount owed and make these loans even more horrific . . .