Student loans are complicated. If you’re going to be successful in paying them off, then you’ve got to make them a little less complicated—otherwise, you’ll never be able to come up with a plan of action.

To make things a little bit easier, I decided to pull together this quick primer explaining all the little bits and pieces that go into a student loan. Just think of it as an anatomy lesson and you’ll do fine!

Need help keeping track of your student loans? Download our free Student Loan Spreadsheet!

What makes up a student loan?

When you get your student loan bill or statement in the mail or check your account online, you’ll first see a screen like this when you log in. (Keep in mind that the exact layout will be different depending on who your student loan servicer is. Most of my loans are through Navient, and there’s a good chance yours are too.)

This screen is called your “Account Summary.” The important information here is:

- Lender or Servicer: In this case, it is Navient, but it could be any of a number of other lenders or servicers.

- Account Information: This includes the account holder’s name and account number, which you’ll need if you ever need to contact your servicer.

- Total Payment Currently Due: This will show you the current payment that you must make. If you are enrolled in autopay (like I am) then you will likely see $0 in this field.

- Loan Snapshot: This is a quick summary of your loans including the due date for the next payment, the amount due at that time, and the status of your loan.

- Total Loan Balance: This s the total amount of money that you owe on your student loans. Note, this may be different from your “payoff amount” (the amount of money you would need to pay to close out your loan). This is because if you pay by check, interest still accrues while your check is in the mail.

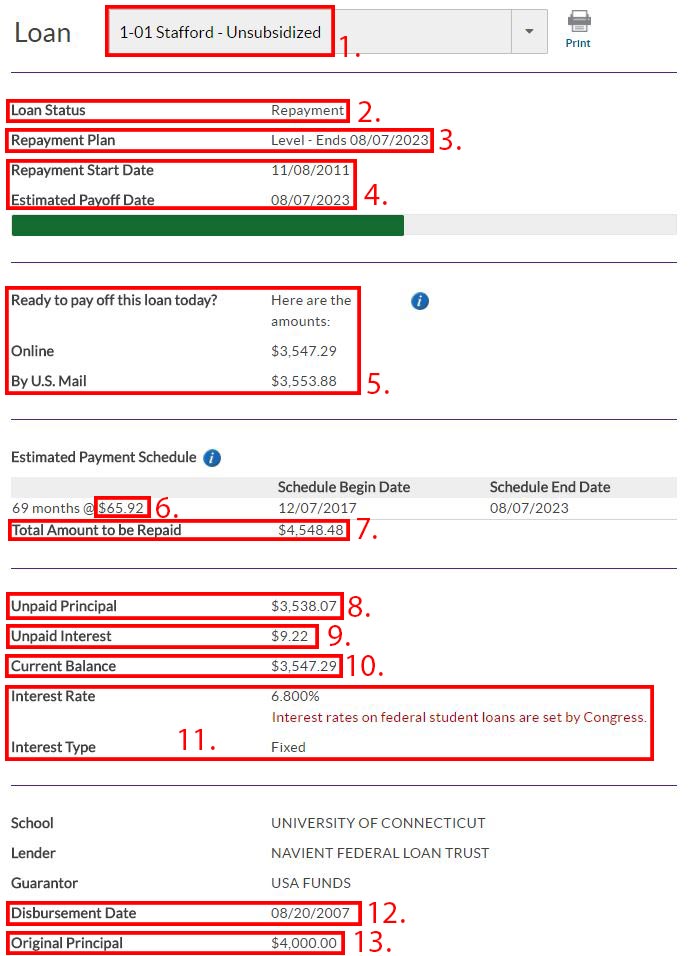

Clicking into an individual loan will show you a screen like this, which contains the details of your individual loan.

This screen is called your “Loan Details,” and this is where you will see all the components of your loan:

- Loan Name: This is pretty self-explanatory, don’t you think? If you have multiple loans, they will assign names to your loans to make it easier for you (and them) to manage. As you can see, the name will often contain important details like whether the loan is subsidized or unsubsidized, and what kind of loan it is (if it is a federal student loan).

- Loan Status: This field will show the current status of your student loan. Mine shows that it is in repayment, but it could also display “Deferral,” “Forbearance,” “Past Due,” or “Delinquent.”

- Repayment Plan: This field shows you your current repayment plan. Mine is in “Level” repayment, meaning that I pay the same amount each month for the life of my loan. If you are in an income-based repayment plan, then this field will describe your payments.

- Repayment Start and End Dates: These are the dates that you started making payments on your student loans and when you are expected to make your last payment (as long as you do not miss any payments or otherwise fall off track).

- Repayment Amount: This is the amount that you must pay if you want to pay off your student loan right now. Making the payment online will be cheaper than making a payment by check, since an online payment is instantaneous while a check must be mailed to your lender or servicer. For this reason, you’ll often see two different amounts based on payment method.

- Monthly Payment Amount: Somewhere on the screen you should see your monthly payment amount. As you can see, this might be buried amongst other information.

- Total Amount to be Repaid: This is the total amount of money that you will pay towards your student loan if you follow your current repayment plan. Changing your payment plan so that you are paying less each month, missing a payment, or placing your loan into deferment or forbearance will all cause this number to go up; paying more each month (or as a lump sum) will save you money and cause this number to go down.

- Unpaid Principal: This is how much of the original loan (principal) you owe.

- Unpaid Interest: This is the amount of interest that has accrued on your student loan since your last payment. When you make a payment, it is first applied to the unpaid interest. The balance of your payment then goes towards paying down the principal.

- Current Balance: This is your unpaid interest plus your unpaid principal.

- Interest Rate and Type: The interest rate is what you are charged for borrowing your student loan. In this case, my loan has an interest rate of 6.8%. That means that, over the course of one year, I am charged 6.8% of the outstanding principal on my student loan. Interest Type can either be “fixed” or “variable,” which we discuss below.

- Disbursment Date: This is the date that your loan was originally taken out to pay for your college expenses.

- Original Principal: This is the original amount that you borrowed, before interest started to accrue.

That’s a lot of information, I know. But it’s really important for you to understand exactly what makes up your student loans, or else you’ll never be able to come up with a plan to pay them off. I highly recommend that you keep all of this information in a student loan spreadsheet that you use to keep track of your student loans from month to month: Doing so means that all of the important information about your student loans is in one place, which is really important if you’ve got more than one lender or servicer.

Free Student Loan Spreadsheet

Back to the Basics

The first step in defeating any enemy is knowing what they’re made of so that you can identify their weaknesses. In the case of student loans, the key parts of their anatomy are the principal, the interest rate, the monthly payment amount, and the loan type. Everything else is gravy that’ll help you crush your debt.

If you’re looking for more information about student loans, check out our student loan basics page, which explains all the different kinds of student loans you might encounter and how you can create a plan of attack to pay them off.

Really terrific breakdown. A lot of people don’t really understand how a student loan works, so this is definitely helpful for folks who are just trying to understand the basics of it.

Thanks! That was my inspiration. When I first graduated from college, I didn’t know any of the different components that made up my loans, and I have to admit, it was definitely rough goings for a while haha.